Been There Done That

If you lost money in the recent market decline, I know exactly how you feel. In 1968, I made my first investments in 3 Mutual Funds. By the end of the year, I had a significant profit, and I knew that I was good at investing. In 1969, the stock market began to decline, and it did not stop until May 1970. I lost more than half my money! I sat there with my teeth in my mouth watching my assets melt because I did not know what else to do.

I felt stupid not only because I thought I was an investor, but also because I was a licensed stockbroker and Insurance agent. I was supposed to know this stuff! The market recovered, and I increased my profits by investing borrowed money. Now, I was a sophisticated investor. In January 1973, the market started to drop and did not stop until December 1974. Again, I sat there with my teeth in my mouth and watched my assets melt. At the bottom of the market, I owed the bank more than my assets were worth. Then, I not only felt stupid, I had no money!

Fortunately for me, I could not blame someone else for my failure. I used my background as a Physicist and Mathematician, and by 1976, I had actually figured out what to do based upon previous market periods. However, when I applied the theory to later market periods it produced vague and unreliable predictions. It took me more than 22 years to figure out what was making the theory appear to be unreliable.

Over the years, I have learned a lot more than that!

Tools of the Trade

You do not control investment markets, but you do control how much you invest, where you invest, and when you invest. There is no way to avoid risk, but you can avoid the consequrences of that risk if you do your Financial Planning correctly, That means using the Tools of the Trade correctly. You know those tools as investments, but to a skilled Financial Planner, they are the tools which help you achieve the financial results that you want.

Each investment has advantages which help you, and disadvantages which can hurt you. Which investments are best is determined by when you want the results and by whether your intentions can tolerate the other consequences of that investment.

Obvious concepts in planning

If you planned a picnic on Saturday, and the weatherman predicts that it will rain, that is a bummer! If you planned to paint the bathroom floor on Saturday, you do not care if it rains because you had nothing planned outside. What you want to do and when have a large impact on your ability to succeed.

When you paint that bathroom floor, you start at the back and finish at the door so that you have a way to get out of the bathroom before the floor paint dries. Thinking about the consequences before you start can avoid problems.

Those two concepts are opbvious, but most people do not think in those same terms when it come to investing. People are always asking,"What is a good investment?" I have to ask them what result do you want, and when do you want it!

TIME is your best friend or your worst enemy

The time between now and when you want the results determines the amount of TIME available for the investment to “mature” so that you can pay the bill for what you want.

Anything is possible, but.....

Stock market investments may not mature in less than 15 years. If you want something in less than 15 years, the stock market could be disappointing - perhaps very disappointing. You should not save your money in the stock market in order to pay that bill which comes due in less than 15 years.

Bond market investments may not mature in less than 10 years. If you want something in less than 10 years, the Bond market could disappointing - perhaps very disappointing.

You should not save your money in the Bond market in order to pay that bill which comes due in less than 10 years. Guarantees are the only reliable investment for financial goals in less than 10 years

Where did I get these rules?

You will not find these rules anywhere else because I invented them. i spent almost an entire month in the basement of the Carnegie Library looking through old Wiesenberger manuals for the performance data of Mutual Funds. Wiesenberger was the "Bible" for Mutual Fund data since 1940. To that data, I added more data from another source Fundscope, and finally, Morningstar.

I used that data to compile an Index of average Mutual Fund performance. One Index for Stock Funds, another for Bond Funds, and a third for Junk Bond Funds. The Indices represented what was possible in the markets - what professional investment managers with diversified portolios were able to achieve.

Using the Indices, I compounded the performance for periods ranging from one year to 85 years in order to measure what an investor could reasonably expect from the markets with professional management and diversified portfolios.

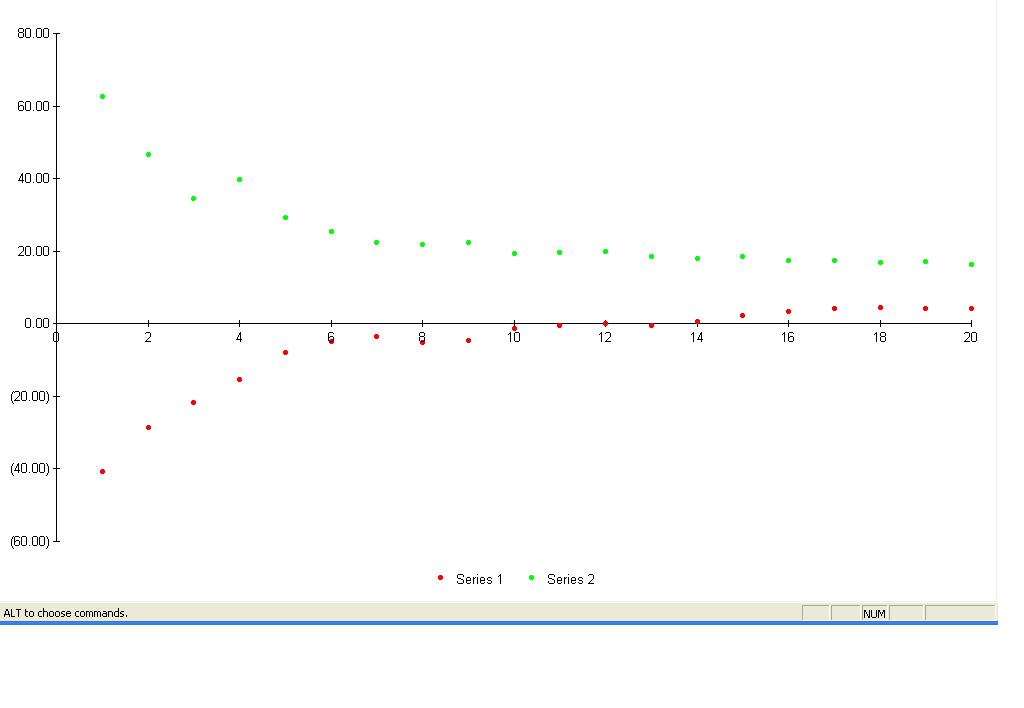

The stock market Index is below. The best performance is on to, and th eworst performance is on the bottom. Some people will argue that all the worst performances occurred suring the Great Depression. Au Contraire! The worst 11 year period ended in 2008.

Best & Worst Stock Mutual Fund Performance for various # years

You do not have to be a genius to see from the graph that investing in the stock market could be disappointing for periods less that 15 years. So you plan on not depending on your investments in the stock market during the next 15 years. You do not care if the market is down in the toilet now, because you were not counting on that money to pay your bills now!

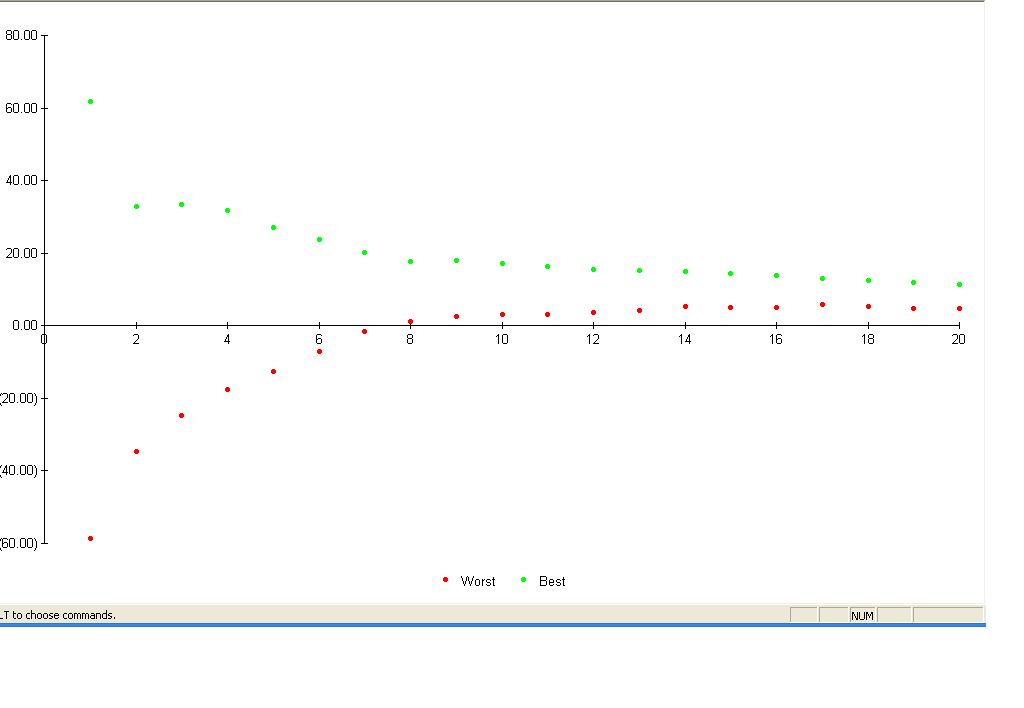

Best & Worst Junk Bond Mutual Fund Performance for various # years

Junk Bond Mutual Funds never lost any money over periods 8 years or longer. However, the worst 10 year result for Junk Bond Funds was 3.21%. You could probably do better than that with a Bank CD or a Fixed Deferred Annuity for 10 years, and they are both guaranteed. As a result, I concluded that I would not use Junk Bond Funds for investments which mature in less than 11 years.

The fact that the stock Mutual Funds never lost money for periods of 15 years or more does not mean that it cannot happen in the future. Similarly, the fact that Junk Bond Mutual Funds never lost money for periods of 8 years or more is no guarantee that it will not happen in the future. The past cannot predict the future. All that we are deciding here is that we will avoid the Stock Mutual Funds for periods less than 15 years, and we will avoid Junk Bond Mutual Funds for periods less than 10 years.